💱Real Rates Continue to Matter Despite Middle East Conflict: Cable FX Macro

- Rosbel Durán

- Apr 2

- 1 min read

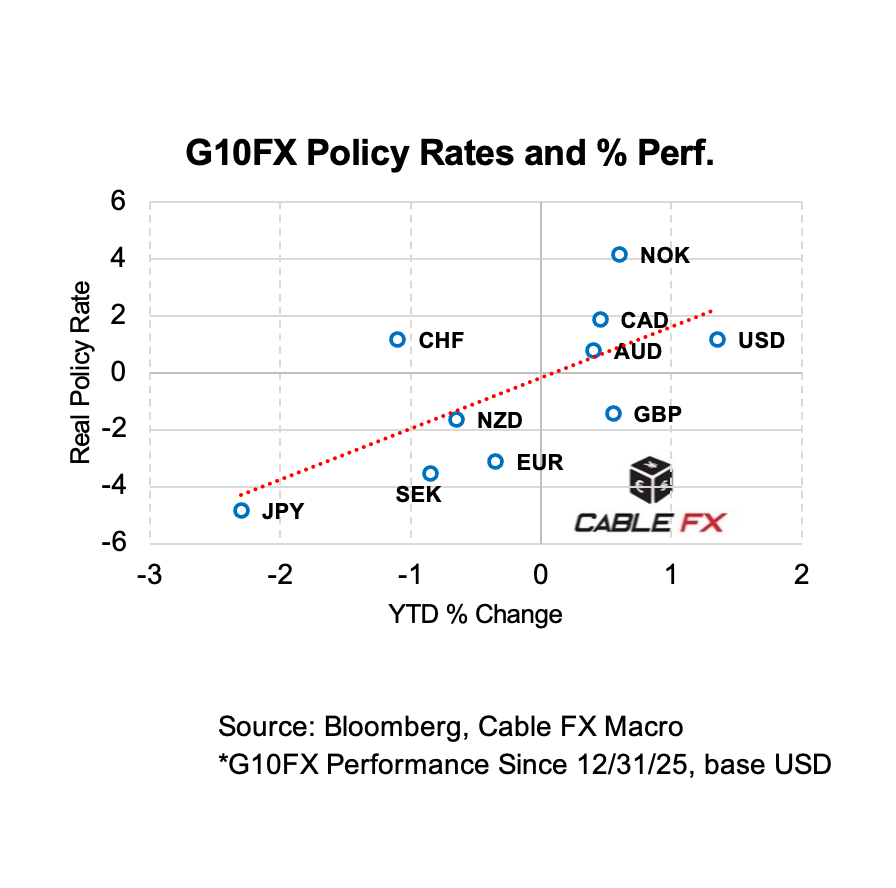

Real policy rates — calculated as the latest nominal policy rate minus headline CPI — remain one of the strongest fundamental drivers of G10 currency performance in 2026. The chart below includes data up to April 2, 2026. I continue to see statistical relevance in the Q3 sample. This is beacuse higher (or less negative) real rates tend to attract capital inflows, support carry, and reinforce currency strength, especially during periods of geopolitical stress like the current Iran conflict and oil shock.

Currencies with the highest real policy rates (NOK, CAD, AUD, GBP) have collectively outperformed the G10 average by a wide margin. The top four real-rate currencies are the only ones showing net positive or near-flat YTD performance vs USD. EUR, SEK, NZD, and especially JPY (with the most negative real rate) have been the clear laggards. This reflects classic carry-trade dynamics: investors demand compensation for holding currencies where policy is not keeping up with inflation.

Real policy rates have been the single best explanatory variable for G10 FX moves year-to-date. Investors positioning for continued energy volatility should continue favoring the highest real-rate currencies (NOK, CAD) while remaining cautious on deeply negative real-rate names like JPY and SEK.

Comments